I am getting confused about how to work out tax on dividends at the higher rate, please help. Sorry it's a bit long.

HMRC website says:

"If you pay tax at the higher rate

You pay a total of 32.5 per cent tax on dividend income inclusive of tax credit where this falls above the basic rate Income Tax limit (£32,010 for the 2013-14 tax year). In practice, however, you owe only 25 per cent of the dividend paid to you after the tax credit has been taken into account".

(1) I'm confused about the 25% when in fact 32.5% minus 10% (tax credit) = 22.5% (and not 25%). Which figure do I use?

(2) My clients wants to move away from paying himself a salary to paying dividends every month (and £640 as monthly wages). Assuming he got £120,000 for the year as dividend income, will the tax on dividend be £120,000 - £32,010 = £87990 x 25% = £21,997.50 ??

(3) Is it acceptable to be doing dividend vouchers every month? and if so, would the dividend voucher be (assuming he gets £10,000 every month as dividend) = £10,000 x 75%?? assuming the 25% instead of the 22.5% in (1) above. I know that dividend paid is 90% of the dividend income but I'm not sure whether this applies to even the higher rate tax payers (hence the 75%) or only applies to the basic rate payers?

(4) On Self Assessment, will total income be (£640x12=£7680) £7680 + £120,000 = £127,680 and is this the figure (£127,680) from which we will again deduct the income tax limit of £32,010 to calculate tax (£127,680 - £32,010)? What's confusing me here is we keep taking away the £32,010 (from dividend income and then again from total income).

On a quick calculation I get it to £23,062 tax payable.

Why are you putting through salary of £7680 when there is no personal allowance?

p.s. ensure that the client is not caught by IR35 before allowing them to get excited about thinking that dividends are an option.

p.s.2 amended only to add the IR35 bit.

-- Edited by Shamus on Wednesday 5th of February 2014 01:29:07 PM

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

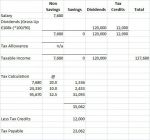

no matter how simple the tax calculation I always slot the figures into a standard tax pro forma.

My assumption was that due to the way that you phased part (3) of your post the £120k was already grossed up so the ungrossed figure was £108k.

Personal allowances are phased out above £100k (the calculation is PA-(50% * (Adjusted Net Income - 100k)))

Here's my calculation :

HTH,

Shaun.

p.s. when calculating the adjusted personal allowance for higher rate tax payers remember that it can only ever be reduced to zero, it cannot be negative.

-- Edited by Shamus on Wednesday 5th of February 2014 01:51:05 PM

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

No problem Tammy but before deciding to go completely down the dividends route don't forget that Dividends are from taxed profit where salary is an expense so the client will still pay corporation tax on the dividends (so tax is just moved from one place to another).

The real saving is National insurance (EMPE & EMPR) but one could risk Pension rights by paying so little in salary that one avoids NI.

Also what about contibutory Pensions? There are types of Pension paid by the company rather than the taxpayer (Executive Pension Plans) Also, Personal Pension contributions will extend the lower tax threshold.

Also if taxable income can be brought below £100k the taxpayer would not lose their personal allowance as they are doing at the moment.

Advise your client that with the sort of income that they have here they need to see an accountant and possibly Independant Financial Advisor in order to ensure that they have had the best available tax planning for their particular scenario as its nowhere near as simple as assuming that putting everything into dividends is the best answer.

HTH,

Shaun.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

Matt, I don't consider having monthly dividends a problem. I normally tell clients to pay their salary monthly and to have a reference on the bank statement as 'salary' and their monthly dividend with the reference , you've guessed it 'dividend'! This shows HMRC that the intention of a dividend is clear. Monthly meetings with minutes saying the dividend was declared and a dividend voucher completely wraps things up. But there is no reason apart from the inefficiency why you can't have a daily dividend if you so wished.

.

.