I have taken over a Business which is a going concern but I setting it up as my own company (only brought the Fixtures and Fittings)

I understand the VAT Threshold is £79000 but I anticipate I will reach this in the next four months.

For example If I reach this threshold on 21st October 2013 and become VAT registered from 1st November 2013, would I need to treat all of my June-October Sales/Expenses as Vatable? Or can I just start accounting for VAT from the date of registration?

(a) You must register when you expect to go over the limit within the next 30 days so taking the example where you expect to go over the limit on the 21st of October you should inform HMRC before the end of that 30 day period (between 22nd of September and 21st of October) and registration is valid from the start of the period (22nd of September).

See this page for what to do about your VAT during the period waiting for your VAT number :

(b) If exceeded by surprise (a massive order appears out of the blue that could not have been pre-empted) then notify HMRC within 30 days of the end of the month in which the limit is exceeded.

You will in this instance be registered from the end of the month following the one in which the limit was exceeded.

Again you may be in a position where you need to be charging VAT before you get your VAT registration number so again, refer to the above link.

Talk to your accountant about the small business VAT schemes (Cash Accounting / Annual Accounting / Flat rate Scheme) which may (or may not) be financially beneficial options for your business,

kind regards,

Shaun.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

Shaun - not sure if reading your 30 day comment wrong but does it not mean if you expect your sales in the next 30 days alone to be more than £79k that you need to register from today. Therefore you dont count anything before today just what you expect the sales in the period 6 June to 5 July to be.

Michael re your query

If your sales exceed £79k in the 12 month period (or less) to 21 October 2013 then you need to be registered for VAT from 1 December 2013 (start of the month after when you go over the threshold). If you havent had your VAT number through by 1 December 2013 you should still issue your sales including VAT and say to your customers that a VAT invoice will follow in due course.

Re pre VAT registration sales and purchases/expenses. You dont need to do anything with your sales pre 1 Dec 2013. Re purchases/expenses you can reclaim VAT on goods bought up to 4 years before registration and services bought up to 6 months before registration. To do this you still need to have the goods at registration or have the service still to be expended (which is usually quite rare). In most businesses what they will have is assets (in your case the fixtures and fitting plus anything you have bought since you set up and stock. If VAT was charged on these you can reclaim in your first VAT return provided you still have them at 1 Dec 2013.

If you have just bought the fixtures is it really a purchase of a going concern? If a transfer of a going concern you will need to take into account the turnover of the previous business under the 12 month rule for VAT.

Someone more experienced in VAT may be able to correct me if any of the above is wrong.

no, I mean that if the treshold is breached in the next thirty days, not £79k within 30 days.

Much as I try I cannot read my post the way that you did but then again, maybe I'm reading what I think that wrote rather than as others may read it.

I think that the first part of your answer said exactly the same as I did but you were going with the hit it then register (my option b) rather than the forward planning approach of (a) which to my mind is the better option without so much of the risk of messing clients around with replacement invoices.

kind regards,

Shaun.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

But my point is that the 30 day rule only applies if your sales in the next 30 days are expected to be more than £79k alone. Not that you breach the £79k in the next 30 days taking into account the previous 12 months.

Might be wrong but that is my intrepretaion of the 30 day rule.

But my point is that the 30 day rule only applies if your sales in the next 30 days are expected to be more than £79k alone. Not that you breach the £79k in the next 30 days taking into account the previous 12 months.

Might be wrong but that is my intrepretaion of the 30 day rule.

Mark

That's how I understood it as well.

__________________

Never buy black socks from a normal shop. They shaft you every time.

Not sure where my explanation is coming off the tracks but its obviously me as there are now two people misunderstanding it...

Right, I sense an example coming on to try and illustrate my point.

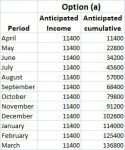

Lets take a nice simple start of April to end of March period.

First option (a)

there's nice steady £11.4k pcm meaning that breach is expected in October.

At the end of September VAT limit is expected to be breached in the next 30 days. You inform HMRC within the 30 days between start of the period and the date of expected breach and you are VAT registered from the start of the period.

This could be thought of as preemptive planning.

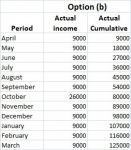

Now option b which I'll be honest is the more common approach where clients are either caught on the hop by the breach or have just been ignoring future events to concentrate on the moment.

Lets keep the breach at October but assume that the breach wasn't expected until December.

In this instance the October Breach is a surprise then HMRC must be informed within 30 days following the end of the month of the breach. So in the example they would be informed by the end of November and VAT registration will run from the start of December rather than the start of October as in option (a).

This can be thought of as a reactive option.

Which option is right for the client is very much dependant upon circumstance but as there are two months difference in VAT take for HMRC between the two approaches I could imagine that an inspector could if they so chose get a little stroppy where there is a distinct income pattern such as a long term contract.

Hope that this clarifies my position and if you re-read the first note with the example in mind you will see that I have not changed my position at all from my original reply.

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

Are you sure that you have the right paragraph number Tim.

I'm looking at this for 4.3 :

4.3 Can I claim VAT relief if my customer has not paid me? If you make taxable supplies of goods or services to a customer for which you are not paid, you may be able to reclaim relief from VAT on the bad debts. You can find out more about this in Notice 700/18 Relief from VAT on bad debts.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

Hate to admit it but I've never actually seen a whole episode of red Dwarf so no idea who the characters are.

Whose Rimmer, whose lister, and why?... Bet this loses something in having to explain it.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

Rimmer is the authoritative one - forever quoting Space Corp Directives by their number but not elaborating. It normally turns out he has quoted the wrong one. It does lose something while translating.

Here's an example - skip to 1:30 (the ones before that are correct ones). http://www.youtube.com/watch?v=DjDd-T8IXsk

__________________

Never buy black socks from a normal shop. They shaft you every time.

I watched all of them. BKN definitely needs a site rule about sniffing the saddles of womens excercise bikes.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

I have end up watching quite a bit of red dwarf over the last 2 years on box set, hadn't planned on watching any when somehow when they put it on I end up watching some of it. I have to admit even though its not really my cup of tea it is really funny when you watch it and get into it!

I own absolutely no Red Dwarf on DVD (or Blu-Ray). I must correct that at some point.

Meanwhile, I now have the theme song on repeat in my head. Well, the first two verses anyway, because I can never remember the rest (I think the shorter/two verse version was probably used for most of its run).

* wanders off singing about being shipwrecked and comatose.

__________________

Vince M Hudd - Soft Rock Software

(I only came here looking for fellow apiarists...)

Going back to your examples above none of them would result in the 30 day rule applying.

See the following from HMRC website

"If your turnover of VAT taxable goods and services supplied within the UK for the previous 12 months is more than the current registration threshold of £79,000, or you expect it to go over that figure in the next 30 days alone, you must register for VAT"

The 30 day rule would only apply if in the next 30 days you expect the turnover in those 30 days alone to be more than £79k. You ignore what has happened in the past.

Shaun in both your examples you would apply the 12 month rule. You would need to notify from the end of October and be charging VAT from the 1st December.

Hopefully a VAT/tax expert will be able to confirm my understanding as this is how I have always understood it to apply ie that the 30 day rule hardly ever applies in practice. Only applies to something that will have large sales in a 30 day period.

The following link also confirms the 30 day rule treated in isolation

Well, I've read it and you're right but I've got to read around this as I'm left scratching my head at the moment as to why I misunderstand this.

-- time passes as reads around the subject --

right, think that I've had a bit of an epiphany.

Seems I've spent all this time reading what I thought it said rather than what it actually said.

Whilst logically it seems that breaching the limit in one month alone still means that the cumulative figure is breached raising the question that why would they even bother including the alone line?

The difference seems to be between the historic test of the cumulative position to date and the future test of what one expects to happen in the next 30 days alone... At the end of which of course it would just be an historic test anyway.

And that was when the penny droped as to my misunderstanding.

Using the historic test registration will not happen until the end of the month following the one where the limit is exceeded (so in this case the start of December) but using the future expectation test VAT registration is retrospective to the start of the period in which the limit is expected to be breached (so in the case in question the 21st of September).

And as you state Mark, a test that will seldom be used.

Whilst it makes no difference to any case that I have ever been involved with I'm certainly glad that this thread cropped up as my understanding of the future test was incorrect and I was in reality simply extending the historic test.

Darn it all, 24 years now I've been playing with VAT and still I find something like this that I misinterpreted!

Many thanks for pointing out that I was wrong Mark, Peasie and Tim, thats now certainly an ingrained bit of knowledge,

kindest regards,

Shaun.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.