Remember that the basic principle of accounting is that all the debits and credits must add up to the same total, so when you debit something, you credit something else.

So, why is money coming in entered as a debit? Because it's debiting one thing and crediting something else - so it's also being entered as a credit.

What it's crediting may be sales, or it might be a customer paying off a debt, and so on: The credit is to sales, (or the sales ledger or something else that's showing a debit balance), while the debit is to the bank account.

And similarly, for money going out: it's a credit on the bank account, and it's debiting something else - such as purchases, or the purchase ledger (it's paying off a credit balance).

Then you can get into deeper stuff, like wot Shaun said.

Edit: Must remember not to use HTML.

-- Edited by VinceH on Tuesday 8th of October 2013 02:47:27 PM

__________________

Vince M Hudd - Soft Rock Software

(I only came here looking for fellow apiarists...)

I started level one C and G book keeping course last night and I am so confused! Please could anybody explain to me why in book keeping money coming in is entered as a debit and money paid out is entered as a credit? I am sure I have completely missed the point here, but I just do not understand the logic behind it. If anybody could explain in a way a 'dummy' could understand, I would be so grateful.

Imagine a scenario where you loan a business £1000 so you need to record capital introduced to the business (which is money owed to the owner of the business) and record where that money went.

At all times you must keep the accounting equation in balance.

Everything you do rotates around that one simple concept (well it would be simple if there were not several different ways of presenting it) that Capital = Assets - Liabilities.

So lets look at what we've done.

Cr Capital account £1000 (money is owed to the owner of the business)

Dr Bank account £1000 (Money is a current asset on the balance sheet)

The accounting equation is happy in the £1000 = £1000 - 0

Now do that in reverse

The owner takes £400 back out of the business so :

Cr Bank £400

Dr Capital account £400

The accounting equation is now £600 = £600 - 0

As you get further into your studies and relate what you are doing to the two halves of the balance sheet the reason for the accounting equation to be in perpetual balance will become crystal clear.

The key to understanding double entry is to always remember an anchorage start point which would generally be the capital account. Remember that money introduced there is a credit and everything else will slot into place.

Hope that helps and my appogies if the explanation was too simplistic.

kind regards,

Shaun.

__________________

Shaun

Responses are not meant as a substitute for professional advice. Answers are intended as outline only the advice of a qualified professional with access to all relevant information should be sought before acting on any response given.

I think also what she means Shamus is what I tried to get my head round when I first started. The 'Bank Statement blindness!'

Helen your used to seeing DR/CR on your bank statment yeah? CR meaning money in, DR money out.... Try to think of this... Your bank statement is a record of what your BANK has on your account. So you the client/customer see THEIR records on you. Now imagine YOU are the bank, everything is switched around. This is the 'accounting' way of showing transactions, DR money in, CR money out (the reverse of what you see above! :) )

Its hard at first, but once you understand and get over the 'Bank Statement Blindness' it will make perfect sense! honest!! I was in same boat to start with, but now its all second nature! :D

Thank you all for your replies, I am sure I will get my head around it eventually, thank you once again for taking the time to help.

Many thanks, Helen

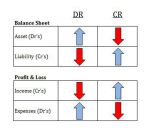

Learning Debits and Credits is frustrating - but trust me there will be one day when it will 'click' and you will be able to apply the principles in any circumstance.

I used to teach my trainees this way (which helped me) - Picture attached.

So, if Assets increase it is a DR and if they reduce then it is a CR

For the bank account, A receipt will mean the bank balance increasing and lets say Sales increasing, so DR Bank, CR Sales

Or lets say a VAT payment, The bank account reduces and so does the VAT liability so DR VAT, CR Bank

use the image attached and I guarantee it will 'click' very soon